How Much Tax Do I Pay on Rental Income? Landlord Tax Brackets Explained

Contents

Table of Contents

The price tax landlords pay on rental income depends on four things: your net profit after deductions, your personal income tax bracket, how many days the property was rented, and whether the IRS classifies your activity as passive rental income or active business income.

Getting those four variables wrong means either overpaying or facing a penalty notice.

How to Estimate Your Taxes on Rental Income

There's no separate federal rental income tax bracket. Net rental profit gets added on top of your other taxable income, wages, freelance earnings, anything else, and taxed at your marginal ordinary income rate.

That's why two hosts with identical $24,000 net rental profits can owe completely different amounts. A host with $40,000 in W-2 income lands in a lower bracket than one earning $150,000 from a day job.

A Simple Tax Estimate Using a 22% Marginal Bracket

Assume $24,000 in annual net rental profit, a 22% federal marginal rate, and a 5% state rate. The rough estimate: $24,000 × 27% = $6,480 combined. That's a planning shortcut, not a filed return, deductions, credits, and passive loss rules all shift the final number.

Why Your Effective Rate is Lower Than Your Top Bracket

Your marginal rate only applies to income above each bracket threshold; lower layers get taxed at lower rates. A host in the 22% bracket doesn't pay 22% on every dollar, only on dollars that fall into that bracket.

The effective rate runs 4–8 points below the marginal rate for most middle-income hosts. Don't calculate your bill by multiplying gross rental profit by your top bracket; you'll overshoot badly.

Short-Term Rental Rules That Change the Tax Outcome

The IRS doesn't treat all rental income the same way, and the gap between a long-term rental and an active STR operation is wider than most hosts expect.

Two thresholds drive most of the difference: average guest stay length and material participation.

If your average booking is 7 days or fewer, your property doesn't qualify as a rental activity under IRC §469; it's classified closer to a business, which changes how losses offset other income and how your tax rate on rental earnings applies.

Active STR operators who handle turnovers, guest messaging, and same-day issue resolution often meet material participation tests that passive landlords don't. That distinction matters for loss deductions. Get a CPA to confirm your classification before filing.

When Self-Employment Tax May Enter the Picture

Rental income is not automatically subject to self-employment tax. The exception kicks in when you provide substantial services to guests, such as daily housekeeping, prepared meals, or concierge bookings, shifting income from passive rental to active business income, where SE tax is at 15.

A per-turnover cleaning fee doesn't trigger this; a daily maid service included in the nightly rate does.

Personal Use Days and Mixed-use Properties

Exceed 14 personal-use days or 10% of rental days (whichever is greater), and deductible losses are capped at rental income, eliminating any net loss benefit for that year. Family stays at reduced or zero rates count as personal use days, not rental days.

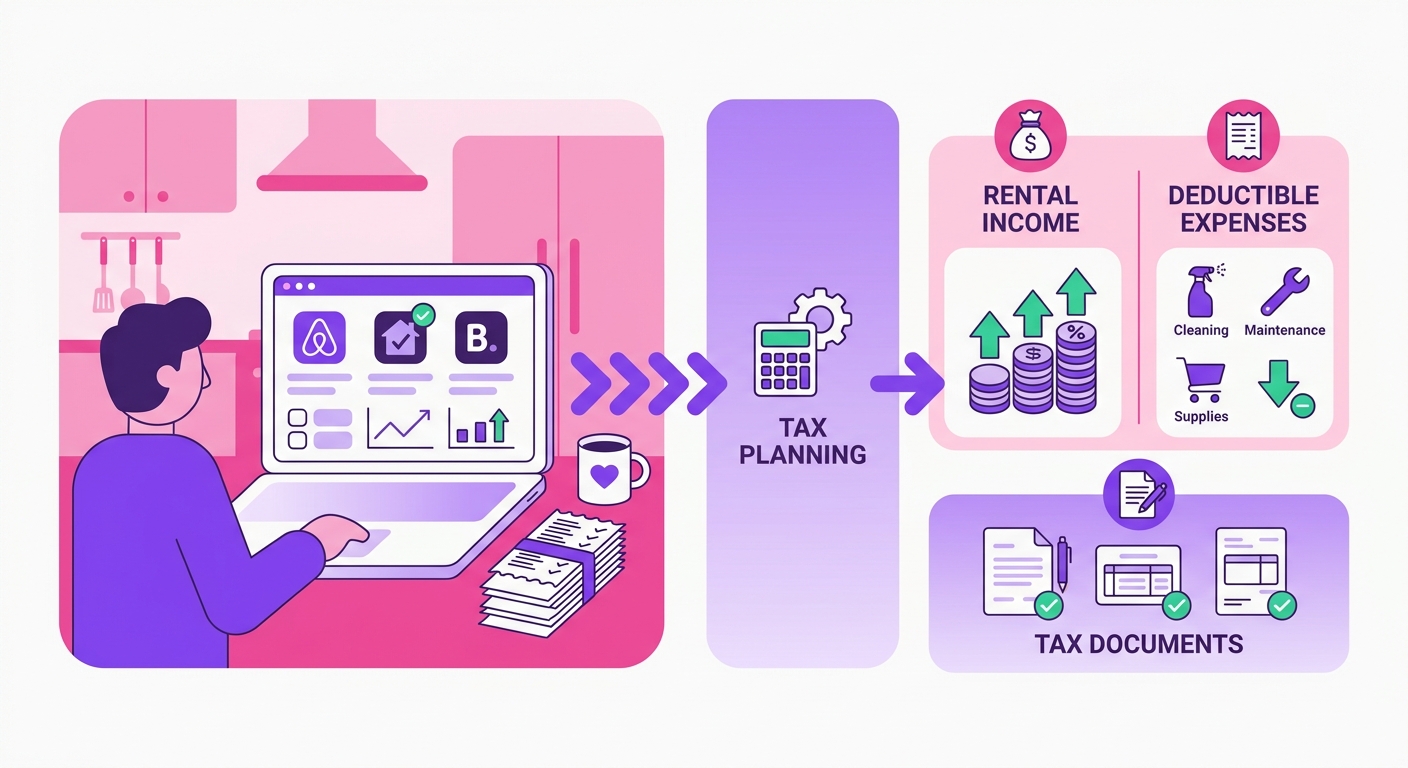

Rental Income Tax Guide for STR Hosts

Rental income is taxable. Your actual bill depends on net profit, your personal tax bracket, how many days the property was rented, and whether the IRS classifies your activity as passive rental income or active business income.

Airbnb, Vrbo, and Booking.com hosts face a compounding problem here: platforms report gross payouts on Form 1099-K, which includes cleaning fees and platform-collected taxes that were never really your income.

The IRS sees the top-line number first. You have to work backward from there, and that requires documentation most hosts don't maintain until they're staring at a tax bill in April.

Why Your Tax Bracket Isn't the First Number You Need

The tax rate tier your rental income falls into is an output, not an input. It's determined by your total taxable income across all sources, W-2 wages, self-employment income, investment returns, and rental profit combined.

A host earning $95,000 from a day job and $18,000 in net rental profit lands in the 22% federal bracket for that rental income. The same rental profit earned by a host with $40,000 in W-2 income gets taxed at 12%. Same property, same revenue, different bills.

This is why the question of what tax rate applies to a landlord's rental earnings can't be answered with a single number. The correct answer is: your marginal rate applied to your net rental profit, after allowable deductions, subject to passive activity rules that may limit how much of that profit you can offset.

The Passive Activity Rule Most Hosts Ignore

If you don't materially participate in your rental activity (more than 750 hours per year in the IRS's definition), your rental losses can only offset other passive income, not your W-2 wages.

This catches a significant number of hosts who assume a paper loss from depreciation will reduce their overall tax bill.

It won't, unless you qualify as a real estate professional or meet the $25,000 passive loss allowance threshold (which phases out between $100,000 and $150,000 in adjusted gross income).

STR hosts who average fewer than 7 days per guest stay may actually be classified as running an active trade or business under IRS rules, which changes the passive activity analysis entirely, but also triggers self-employment tax.

What Counts as Rental Income for Airbnb, Vrbo, and Booking.com Hosts

Most hosts undercount their taxable income, not because they're hiding anything, but because they're only looking at cash deposited into their bank account. The IRS casts a wider net than your payout statement suggests.

These income sources belong on your return:

Nightly rate revenue across all bookings

Cleaning fees you retain (not passed directly to a cleaner as a reimbursement)

Pet fees, extra guest fees, and any host-set surcharges

Cancellation payouts the guest forfeits, and you keep

Platform incentive bonuses and referral credits are paid out as cash

Insurance claim reimbursements that replace lost rental income (property damage reimbursements are treated differently)

Platform Payouts That Usually Belong in Income

Your 1099-K from Airbnb or Vrbo reports gross booking value, which can exceed your net payout. Airbnb sometimes withholds host service fees before sending funds, but those fees still represent income you earned; you just paid a platform expense from it.

On Booking.com, the commission model works similarly: you collect the full amount from guests, then remit Booking. Both the gross receipts and the commission expenses belong in your books, not just the net.

Treat your 1099-K and payout statements as starting records, not the final answer on how rental income is taxed for your situation.

The Deductions That Usually Matter Most for STR Hosts

Deductions reduce your taxable profit, and that's the most direct answer to how much tax you pay on rental income. Every legitimate expense you claim shrinks the amount the IRS actually taxes.

For a property earning $150/night at 75% occupancy ($41,000 gross), the deductions below routinely cut taxable income by 30–50% before depreciation enters the picture:

Platform fees: Airbnb's 3% host fee, Vrbo's 5%, Booking.com's commission, all deductible

Cleaning labor, turnover supplies, and laundry

Utilities, Wi-Fi, and streaming services used by guests

Short-term rental insurance premiums

Mortgage interest and property taxes (pro-rated to rental days if mixed-use)

Software, active pricing tools, photography, and accountant fees

Depreciation isn't just another line item; it's your most powerful tax shield. Seriously, don't sleep on this. IRS Publication 527 is the rulebook, and it lets you depreciate residential rental property over 27.

This simple move can add thousands in annual deductions, like the $11,500 deduction one of our clients claimed, all with absolutely no cash outlay.

Repairs, Improvements, and the Depreciation Trap

Replacing a broken lock is a repair, deductible in full this year. Replacing the entire kitchen is a capital improvement depreciated over time.

When you sell, the IRS recaptures depreciation at up to 25%. Don't let that stop you from claiming it; deferring a tax benefit now to avoid a smaller tax later is rarely the right trade.

Recordkeeping by Payout, Stay, and Expense Category

There's only one bookkeeping system that truly holds up. You must perform a monthly reconciliation for each channel separately.

Pull your Airbnb, Vrbo, and Booking.com payout reports one by one, because their formats are wildly different. Airbnb's CSV, for instance, has 14 columns that don't map to Vrbo's at all. Trying to combine them later is a recipe for disaster. It's tedious, but it's the only way.

Track three buckets independently:

A Fast Estimation Framework for Hosts With 1 to 50 Properties

That's all it takes to get a defensible tax estimate before you call your CPA.

Annualize gross rents. Use total platform payouts for the year, actual deposits received, not nightly rates. A single property at $150 ADR and 75% occupancy generates roughly $41,000 gross.

Subtract ordinary expenses. Platform fees, cleaning, supplies, insurance, utilities, and repairs all reduce taxable income dollar-for-dollar.

Apply rates and STR-specific rules. Federal rental income brackets mirror ordinary income rates (10%–37%); add your state rate. The 14-day personal-use rule, material participation tests, and STR classification each shift tax owed by thousands per year.

Single-property example: $41,000 gross, minus $1,230 platform fees, $3,600 cleaning, $2,400 supplies and repairs, $10,900 depreciation, and $8,000 mortgage interest leaves roughly $14,870 taxable. At a 22% federal rate plus a 5% state rate, that's about $4,015 owed.

Mistakes Hosts Make Before They Hand Numbers to a CPA

The most expensive mistake isn't miscalculating the tax rate applied to your rental earnings; it's handing your CPA the wrong starting numbers. Fix the inputs, and the math takes care of itself.

Taxing gross payouts instead of profit. Your Airbnb 1099-K shows total platform payouts. That's not your taxable figure. Subtract every allowable expense before you report anything.

Conflating lodging tax with income tax. Occupancy taxes you collect and remit are pass-through funds. They don't belong in your revenue line.

Ignoring owner-use allocations. Fourteen or more personal-use days, and the IRS requires you to split expenses proportionally between rental and personal use. Most hosts skip this entirely.

Expensing capital improvements immediately. A new HVAC system isn't a deductible repair; it depreciates over its IRS recovery period.

Forgetting state filing obligations. Rental income earned in a different state from where you live often triggers a non-resident return in that state.

Local STR permit rules are a separate matter from tax treatment entirely. For city-specific operating requirements, the compliance guides cover those details; don't conflate licensing compliance with how your income gets taxed.

When to Get Tax Help and What Numbers to Bring

If your gross rental income crossed $20,000 in 2025, or you have personal-use days that split deductions between Schedule E and Schedule C, hire a CPA or enrolled agent before you file.

Self-filing at that complexity level costs more in missed deductions than the professional fee.

Bring these records to every tax appointment:

Annual payout summaries from each platform (Airbnb, Vrbo, Booking.com)

Itemized expense ledger with receipts

Mortgage interest statement (Form 1098)

Property tax bill

Existing depreciation schedule, if the property was previously filed

Owner-use calendar showing personal nights versus rental nights

Missing any one of these slows the appointment and risks an inaccurate return. Pull them before you book the meeting.

FAQs

Does the 14-day Rental Rule Apply If I Also Use the Property as My Primary Residence?

Yes, but the threshold is strict. If you rent for 14 days or fewer and use the property personally for more than 14 days, rental income is tax-free, and you report nothing. The moment you hit day 15 of rentals, the full year's income becomes taxable, and mixed-use deduction rules kick in, so track your rental nights carefully.

Are Airbnb Cleaning Fees Included in My Taxable Rental Income?

The IRS treats cleaning fees collected through the platform as gross rental income, even though you pass most of that money to a cleaner. Report the full amount received, then deduct the cleaning cost as a rental expense; the net taxable difference is zero, but both figures must appear on Schedule E.

How Does a Co-host's Management Fee Affect the Owner's Rental Income Tax Bracket?

The owner reports gross revenue and deducts the co-host fee as a management expense, reducing net rental income before it hits their marginal rate. On a property earning $40,000 gross with a 20% co-host fee, taxable profit drops by $8,000, a real difference if the owner sits near a bracket threshold.

If Vrbo or Booking.com Withholds Occupancy Taxes on My Behalf, Do I Still Owe Anything?

Platform-remitted occupancy taxes are not your income and don't appear on Schedule E. What matters is whether the platform's 1099-K includes those taxes; Airbnb excludes them, but some platforms don't. Reconcile your 1099-K against actual payout statements before filing, because a mismatch is one of the fastest ways to trigger an IRS inquiry.

Can a Property Manager Filing Taxes on Behalf of Multiple Owners Use a Single EIN for All Rental Income?

No. Each owner's income belongs on that owner's tax return, and aggregating it under a manager's EIN creates a misattribution problem. If you co-host or manage for third-party owners, issue a 1099-NEC for your management fees and ensure each owner receives accurate gross income figures tied to their own Social Security number or EIN.